Good Business Great Stock

If you find a well-run cash generative micro/smallcap, share this article with the management team. Subject: Just Do This!

In 1988, Eddie Lampert launched his fund, ESL Investments. Legendary investor Richard Rainwater invested $28 million in seed capital. The first ten years was mostly traditional stock picking and he built up a good track record. Lampert's investors were prominent individuals like Michael Dell, David Geffen, Ziff family, and the Tisch family.

By the late 1990’s he became more activist in his approach pushing management to make changes. By 2007, his fund ballooned to $20 billion in assets after racking up 18 years averaging ~30% annual returns.

A few years prior he placed big bets on AutoNation and AutoZone which were 25%+ positions in his fund. In 2003, Lampert invested $700 million buying Kmart debt at 20c on the dollar and provided the bankruptcy re-org financing. The debt was converted into equity. Lampert owned 54% of Kmart equity. He was in control.

Lampert had the Midas touch.

Kmart lost $3.2 billion in 2002. Post bankruptcy/Lampert financing Kmart was able to produce $400m in operating profit in 2003, and $900 million in 2004. Also in 2004, Lampert sold 70 Kmart stores (5% of the base) for $900 million to Sears and Home Depot, and Kmart’s stock soared 300%.

The sale gave him the idea that Sears was also an opportunity, and over several months he negotiated Kmart’s purchase of Sears for $12 billion.

Eddie was at his peak. He was on one heck of a run. He looked like he could do no wrong.

In a 2018 Vanity Fair article, Richard Rainwater said of Lampert,

“He’s so obsessed with moving in the direction he wants to move that sometimes people get burned, trampled on, bumped into, I think he has gone about alienating himself from almost everyone who he’s come into contact with.”

Another former colleague said,

“He’s really an extreme guy. There’s something odd about him, I think, his lack of emotional connection to people. . . . It’s so important, but some people just don’t have that. They’re off in their own little world.”

When you are on a winning streak, you want to bet heavier on your next bet because you feel you’ve earned the right.

Sears would become 70% of Lampert’s portfolio in 2007. The position totaled $16.5 billion. 10 years later its value declined by 95%. Sears filed for bankruptcy in 2018, and Eddie Lampert still owns the nine remaining Sears stores scattered around the country.

Most investors remember Eddie Lampert for his one major stumble, and forget about some of the amazing successes.

Let’s dive into AutoZone.

AutoZone (AZO), O’Reilly Automotive (ORLY), and Advanced Auto Parts (AAP) make up 40% of the retail automotive replacement parts market in the United States. These are boring businesses in mature industries, but the compounding lies below the surface. In the United States, the average age of a car continues to rise. As a car ages the maintenance costs go up. It costs $2,000 per year to maintain a car with 50,000 miles, and it costs $4,000 per year to maintain a car with 100,000 miles.

AutoZone, O’Reilly, and Advanced Auto Parts are similar, but the differences are in the nuances. Historically, Advanced Auto Parts caters to the “we’ll do it for you” consumer, while AutoZone and O’Reilly cater to the “do it yourself” consumer. Advanced Auto has been struggling lately and the stock chart tells the tale, but in general all three are very good retail businesses with great margins (55%) and high returns on capital.

In fact, the title of this article isn’t completely accurate – AutoZone isn’t a good business. It’s a low growth great business.

AutoZone’s intense focus on the customer was born in the 1980’s and 1990’s. AutoZone stores were deliberately designed to be light and inviting, instead of dusty, dark, and gloomy. In the 1980’s they were the first retailer to private label parts and give a lifetime warranty, even when the manufacturer themselves wouldn’t provide one. They were the first to offer an electronic catalog in all stores that would allow employees to look up parts, warranties, and check inventories at nearby stores. In the 1990’s, they were the first ones to use satellite technology to connect their stores to their warehouses to increase efficiency. Most importantly, AutoZone employees grew a reputation for always going the extra mile for the customer.

40% of the market outside these major chains is mom and pop mechanics and small auto parts retailers, so the industry has always been ripe for consolidation. In the early - mid 1990's AutoZone acquired a 500-store chain and a 200-store chain and was spending considerable money on refitting the stores. This caught the attention of Eddie Lampert.

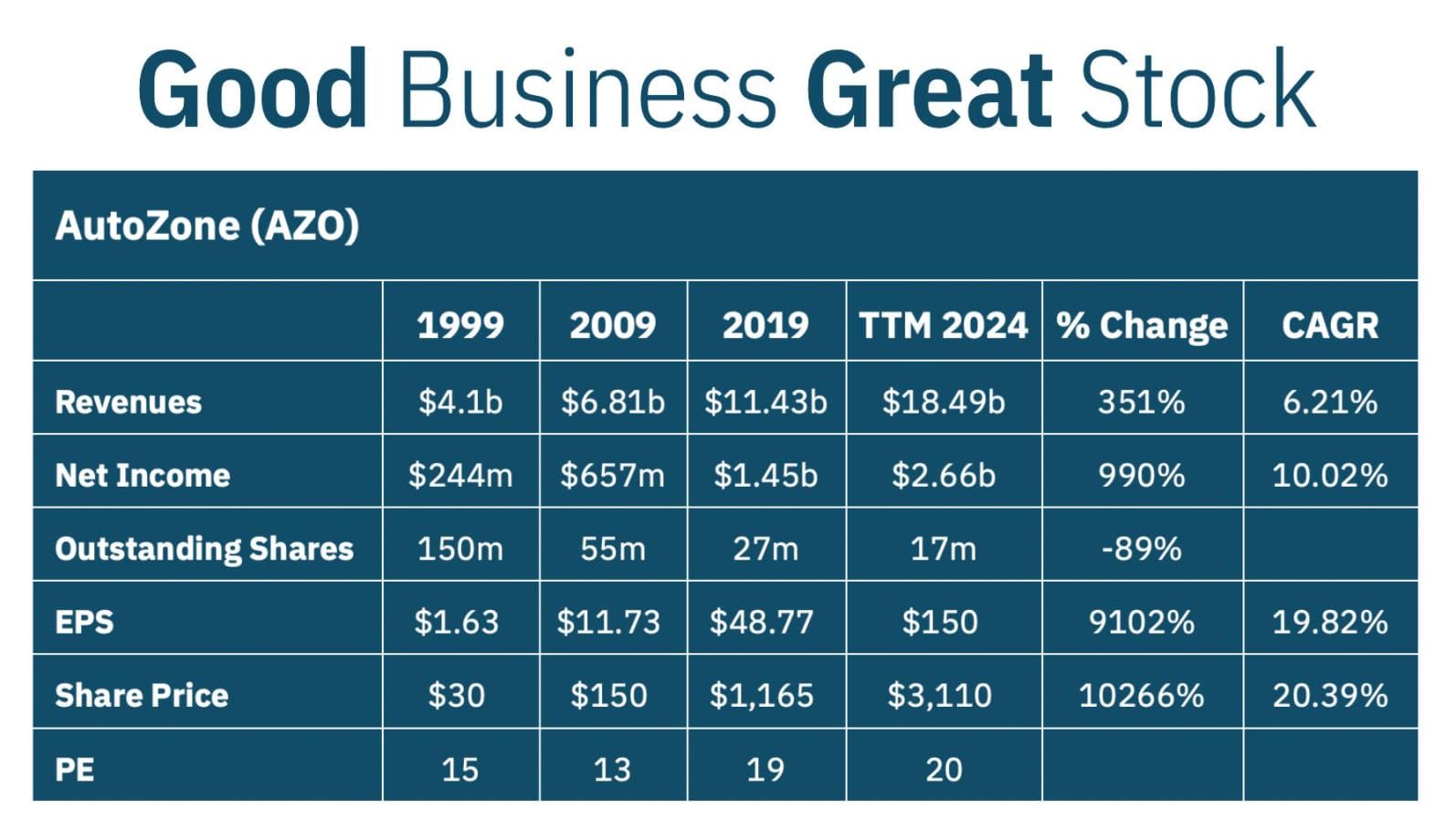

In 1998, Eddie Lampert started acquiring shares of AutoZone. He ultimately acquired 29% of the company and joined the board in 1999. Lampert helped refocus AutoZone away from big acquisitions toward big buybacks and focusing on capital efficiency. Each AutoZone store costs $2.5 million to build out, produces $2 million in annual revenue at 20% operating profit. If you include debt and capitalized leases, it’s close to a 40% ROIC.

To Lampert, what made sense was slow methodical growth (200 stores each year) and plowing all excess cash flow into share buybacks. This deliberate approach didn’t just enhance shareholder value; it reshaped AutoZone’s identity as a company that prioritized creating value over chasing scale.

Eddie Lampert stayed on the board until 2006 and sold out of his position in 2012 making 20x on his investment. He would have made 100x if he held on for another 12 years. Investing is hard, even when it’s easy.

Even though AutoZone has been a 25 year 100-bagger success story, the stock has never been expensive, historically trading between 13-20 PE. With a low revenue growth of a 6% CAGR, the company amplified its EPS growth to over 20% annually. If you do some simple math the buybacks turned a 10% IRR into a 20% IRR. It turned a good outcome into a great one.

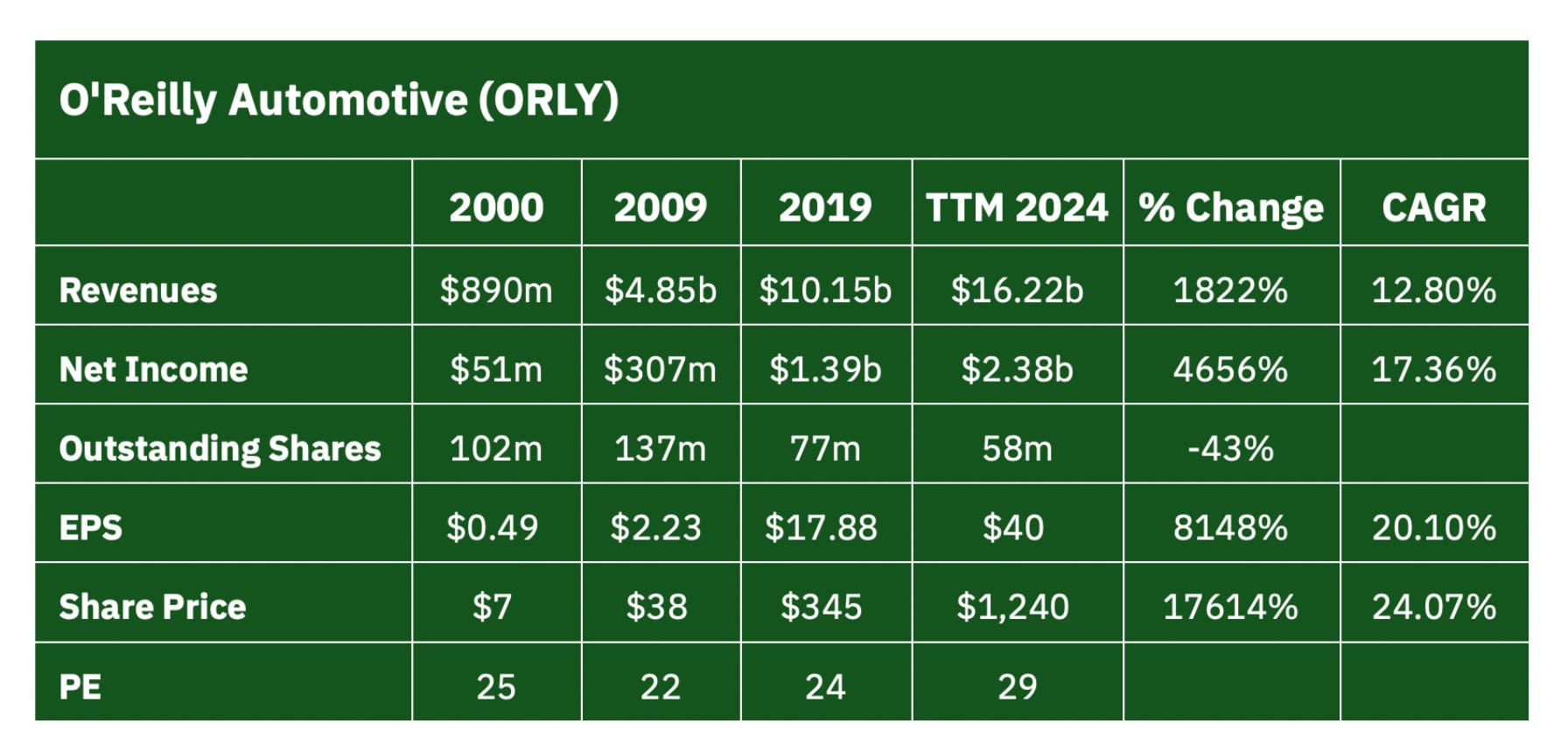

O’Reilly growth rate is double that of AutoZone which has historically given the equity a higher valuation between 20-30 PE. What is interesting is the EPS growth rate is quite similar between the two companies. Both stocks have performed extraordinarily well.

For cash-generative microcap companies, the message is clear: success isn’t about becoming the biggest or growing the fastest—it’s about finding the right size for your business model, industry, and management team. This principle applies not only to the size of the business but also to its shares outstanding. Disciplined share buybacks can provide an invaluable mechanism for creating value when orchestrated in a thoughtful disciplined manner.

Microcaps should adopt AutoZone’s mindset:

- Focus on operational efficiency.

- Use buybacks strategically to compound EPS growth when reinvestment opportunities are limited.

- Avoid the temptation to chase growth for growth’s sake, especially through acquisitions that strain resources or exceed integration capacity.

We live in a revenue growth at all costs type of world. Investors, investment bankers, analysts – they all scream at management teams to grow faster. It takes incredible discipline to turn your back on the crowd and instead focus on EPS growth at all costs.

If you find a well-run cash generative microcap, share this article with the management team. Subject: Just Do This!

You can prove to them there is another way. A slower growth business can still be a great stock.

Interact and learn with 250+ of the best microcap investors on the planet:

MicroCapClub is an exclusive forum for experienced microcap investors focused on microcap companies (sub $500m market cap) trading on United States, Canadian, European, and Australian markets. MicroCapClub was created to be a platform for experienced microcap investors to share and discuss stock ideas. Since 2011, our members have profiled 1200+ microcap companies. Investors can join our community by applying to become a member or subscribing to gain instant view only access. MicroCapClub’s mission is to foster the highest quality microcap investor Community, produce Educational content for investors, and promote better Leadership in the microcap arena. For more information, visit https://microcapclub.com/ and https://microcapclub.com/summit/