The Superinvestors of MicroCap

Microcap gets little attention despite being the small island of investing that produces superinvestors.

In investing, the skeptic says results don’t persist; the past offers little guidance for the future. Conventional wisdom preaches regression to the mean. But occasionally, a big idea comes along potent enough to trump these forces. The idea forges a tribe of believers who congregate in a figurative place sharing ideas and mental models. Their results may seem uncorrelated but zoom out and you find a common North Star and set of principles.

An example is the value investing philosophy of Benjamin Graham and David Dodd, whose ideas bred success for disciples even as academia declared them dead. Graham, a man shaped by memories of the Great Depression, sought a margin of safety in cheap, ignored, out-of-favor stocks. “Treat investing like a business, not a casino,” he said. Have the intelligence to think independently combined with the temperament to act on conviction.

Ben Graham and David Dodd wrote Security Analysis in 1934. The book is widely regarded as the fundamental text for learning about value investing and is considered the "Bible" for value investors. Warren Buffett got an A+ in Ben Graham's class and graduated from Columbia Business School in 1951. He went to work with Graham Newman & Company in 1954 until it closed in 1956. Buffett then launched his partnership.

On March 17th, 1984, Buffett gave a speech at Columbia Business School on the 50th anniversary of Security Analysis. The speech was titled, "The Superinvestors of Graham-and-Doddsville". Buffett profiled several value investors trained by Graham and Dodd who posted incredible long-term track records. These included Walter Schloss, Tom Knapp, Ed Anderson, Bill Ruane, Rick Guerin, Stan Perlmeter, Charlie Munger, and Buffett himself. Though adopting varying investment strategies, they all shared the foundational approach of Graham and Dodd by buying securities trading far below estimated intrinsic value to allow a margin of safety.

Walter Schloss never went to college; he attended high school and night school while working as a clerk. However, he studied under Graham at Columbia Business School and became a star pupil. When Graham closed his investment partnership in 1956, Schloss started his own. Walter’s son Edwin then joined the firm in 1973. During the height of the dotcom bubble, when they could only find three stocks cheap enough to buy, they called it quits. From 1956 to 2001, Schloss's partnership generated a compounded annual return of 15.3% compared to just 10.5% for the S&P 500 over the same period. More about Walter Schloss.

Ben Graham, through his firm Graham-Newman Corp, used Tweedy & Co. as a brokerage. Tom Knapp took a night course taught by David Dodd. When Graham-Newman shut-down, Tom Knapp joined Tweedy and transitioned it from a brokerage to an investment firm. In 1968, Tom Knapp and Ed Anderson teamed up with two others to form Tweedy, Browne. They took the firm from $10 million in capital to several billion.

Stan Perlmeter was one of the lesser-known but highly successful value investors. He launched Perlmeter Investments, Ltd in 1965 and ran it until his death in 2018. Perlmeter managed a modestly sized investment partnership, rarely topping $20 million in assets. However, he generated exceptional returns by sticking to the bargain-hunting methods outlined by Graham. From 1965 to 1984, Perlmeter's partnership returned over 19% per year on average.

Charlie Munger said of Rick Guerin, “We met on the opposite side of a deal in January of 1962, and Rick quickly realized he was on the wrong side. From there we did a lot of deals as co-venturers.” Rick Guerin started his partnership in 1965 and partnered with Buffett and Munger on Blue Chip Stamps and See's Candy. He became overleveraged during the 1973-74 downturn and was forced to sell his Berkshire stock to Munger at $40 per share. Everyone loves to tell the worst part of Rick’s story, but he lived a great life and did quite well. From 1965 through 1983, Guerin's partnership,Pacific Partners generated an outstanding average annual return of 23.6%. Here is a great tribute to Rick Guerin.

Bill Ruane met Warren Buffett when they were both enrolled in Graham’s security analysis course at Columbia. They became good friends and spoke every day. When Buffett shut down his partnership, he advised his clients to move over to Ruane. Ruane launched the Sequoia Fund in 1970 and managed it for over 25 years. From 1970 to 1992, Ruane compounded Sequoia's net asset value at an average annual rate of 14.5% compared to just 10.6% for the S&P 500 over the same period. More about Bill Ruane.

Ben Graham and David Dodd helped pioneer a movement, some would say a religion, that has lasted for decades. Thousands if not millions of investors have been born into this tribe, with many of the greatest investors ever coming out of this camp.

One lesser-talked-about yet lucrative tribe is microcap investing.

Most of the greatest investors ever, including Warren Buffett, Peter Lynch, and Joel Greenblatt, started their careers as microcap investors. It's the only area in the public market where retail investors and small institutions have the advantage over larger institutions.

Microcap gets little attention despite being the small island of investing that produces superinvestors. And yet the proof is all around us, as evidenced by the next generation of superinvestors emerging from our MicroCapClub community.

Both Connor Haley (32.9% Net CAGR since 2018 at Alta Fox Capital) and Daniel Smoak (43.9% Net CAGR since 2018 at Smoak Capital) started posting on our community long before they launched their funds. Michael Melby actively posted soon after starting Gate City Capital Management and has since generated a 22% Net CAGR since 2011. We have dozens of other emerging managers and private investors who are quietly building impressive track records across the globe.

When I started investing in microcaps in the early 2000s, most research and conversations occurred on public stock message boards. Why? Microcaps are mainly owned by retail investors, and this is where retail investors congregated. These forums were where reputations were made. The ability to follow investors, privately message, form relationships, and view historical discussion on a company was powerful. Idea generation, collaboration, discussion, networking are critical components to building community. Call me “old school,” but I still think stock picking communities can be big assets for any stock picker if used effectively. This is why I founded MicroCapClub in 2011.

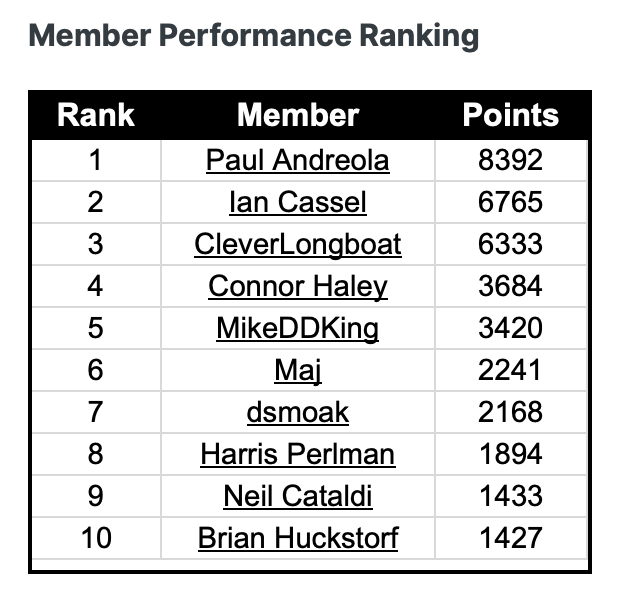

Today, we have 280 of the smartest microcap investors on the planet on our community. We track every company each member profiles and rank each member based on a simple formula. Our Member Ranking System is the aggregate percentage gain (or loss) of every company a member has profiled. If a member has +876 points, it means they've profiled a cumulative 876% of gains across all companies they've profiled. We don't allow members to sell to lock in gains, so it's a coffee-canned ranking calculation. This used to bother me, but over time I’ve come to realize it forces investors to think about long-term returns. The ranking is a simple and elegant way to rank members who have profiled the biggest winners over the long-term. When you join our community, you can follow and interact with members and be alerted every time they post on an idea.

In Hendrik Bessembinder's research, Do Stocks Outperform Treasury Bills?, he studied 26,000 stocks from 1926 to 2015. He was analyzing long-term stock returns, he examined 20 variables. Three of these variables were statistically significant. The most significant variable was net income growth – a similar takeaway to what Jenga Investment Partners concluded in their study of Global Outperformers.

87% of all global equities that went up 1000% or more over the past ten years were microcaps. 82% of those were profitable at the start of their ascent, and 91% had some history of profitability. The key is small, growing, profitable, and undiscovered. This is also why we launched our MCC Profitable Index (MCCPI) earlier this year.

Bessembinder also found that from 1926 to 2015, only 86 stocks (out of 26,000) accounted for over half of the wealth creation.

I’m always reminded of this wonderful quote [Art of Holding].

“The most successful investors I worked with, those who made the most money, all had one thing in common: the presence of a couple of big winners in their portfolios. Any approach that does not embrace the possibility of winning big is doomed.” – Lee Freeman-Shor

The key is finding, buying, and holding the winners, and it’s not surprising our rankings are driven by finding the few big winners.

- Member Paul Andreola, founder of SmallCap Discoveries, profiled XPEL (XPEL) at $0.36 per share on June 10th, 2013, adding over 8,000 points to his ranking. An 80-bagger.

- Member CleverLongboat profiled Celsius Holdings (CELH) at $4.25 per share on July 10th, 2019, adding over 6,000 points to his ranking. A 60-bagger.

- I profiled Napco Security (NSSC) at $2.15 per share on December 18th, 2011, adding over 4,000 points to my ranking. A 40-bagger.

- Member Connor Haley profiled Straight Path Communications (STRP) at $5.58 per share on October 2nd, 2013, adding over 3,000 points to his ranking. The company was acquired. A 30-bagger.

- Member MikeDDKing profiled Biosyent (RX.V) at $0.55 per share on February 17th, 2012, adding over 1,400 points to his ranking. A 14-bagger.

- Member Daniel Smoak profiled HemaCare (HEMA) at $1.00 per share on February 23rd, 2017, adding 2,500 points to his ranking. The company was acquired. A 25-bagger.

- Member Maj Soueidan, founder of Geoinvesting, profiled BlueLinx Holdings (BXC), a 10-bagger, and Koru Medical Systems (KRMD), an 8-bagger.

In fact, our members have profiled 235 multi-bagger stocks since inception. This equates to 1.5 per month since the community was started in July of 2011.

Buffett, Lynch, and Greenblatt all started in microcap for a reason: it’s the only place in the public markets where an astute investor managing small sums has a structural advantage over institutions. Microcap investing has a long history of producing the greatest stock pickers in the world. Microcap is where greatness begins. The next Buffett is likely sifting through the thousands of obscure microcaps that trade around the world. There’s a good chance that person is on MicroCapClub. That person could be you.

Interact and learn with 250+ of the best microcap investors on the planet:

MicroCapClub is an exclusive forum for experienced microcap investors focused on microcap companies (sub $500m market cap) trading on United States, Canadian, European, and Australian markets. MicroCapClub was created to be a platform for experienced microcap investors to share and discuss stock ideas. Since 2011, our members have profiled 1000+ microcap companies. Investors can join our community by applying to become a member or subscribing to gain instant view only access. MicroCapClub’s mission is to foster the highest quality microcap investor Community, produce Educational content for investors, and promote better Leadership in the microcap arena. For more information, visit https://microcapclub.com/ and https://microcapclub.com/summit/