The Hidden Lessons from Monster Beverage Corporation

It's the first 11 years when Monster Beverage was still a microcap that are the most instructive.

Monster Beverage (MNST) has risen 180,000% over the last 32 years, but the stock went nowhere for the first 11 years. Everyone talks about the last 21 years after the breakthrough moment of launching the Monster Energy Drink. No one talks about the first 11 years when the management and business looked mediocre at best. As stock pickers, it’s the first 11 years when Monster Beverage was still a microcap, that are the most instructive.

In 1992, two South Africans, Rodney Sacks (age 42) and Hilton Schlosberg (age 40), acquired Hansen Natural Corporation for $14.5 million. Rodney became the CEO and Hilton became the President. Rodney and Hilton each owned 40% (80% total) of the company. That same year they took the company public on the Nasdaq.

In 1992, Hansen Natural produced $20 million in sales, lost money, and was a $20 million market cap. The company continued to struggle. The losses continued in 1993, 1994, and 1995.

Hansen Natural fell to a $6 million market cap. It was an ugly duckling.

However, the launch of its Smoothie drinks in late 1995 brought renewed optimism. The Smoothie line turned out to be a crucial success, generating one-third of the company's revenue within the first nine months and accounting for one in every five cases sold. This turnaround allowed Hansen Natural to report a profit of $357,000 in 1996.

The company rose back to a $25 million market cap, but it was still an ugly duckling.

At first Sacks was content to chase whatever beverage trend was in vogue, but he knew Hansen's me-too products had little chance of standing out. "We needed to create something different," he recalls.

Hansen's "functionals" came out in early 1997. A functional beverage provides health and wellness benefits from a variety of functional ingredients, ranging from probiotics to caffeine to bioactive proteins. The trend in functional beverages had already been established in Europe, where they first caught the attention of Sacks.

Hansen's functional drinks were lightly carbonated. They were packaged in skinny 8.2-ounce cans, offering a more manageable serving for an energy drink. Each can retailed for about $2, whereas sodas cost 60 cents. They offered "an immediate boost whenever you need it the most."

Another advantage attributed to Hansen was the superior taste of its drinks. The company also benefited from an established distribution network. Hansen aggressively promoted its functional drinks by giving out free samples and setting up literature centers in grocery stores. Initially, convenience stores and liquor stores were the primary retailers of the new beverage, but it quickly gained traction with a variety of other retailers.

By 1997, three-quarters of the company's sales were from California. The success of the functional drinks line helped Hansen increase out-of-state sales of its other products. In 1997 sales grew to $43 million and earnings were $1.3 million.

By 1998, functional drinks accounted for a quarter of Hansen's $54 million in sales, and the company's earnings grew to $3.6 million. The company was a $40 million market cap.

From 1998 to 2002, sales would grow from $54 million to $92 million, but earnings would stagnate around $3-4 million. The stock would go nowhere for five years, stuck at a $40 million market cap.

From 1992 to 2003, Hansen’s stock went up 50%. A 3.75% CAGR. It was still an ugly duckling.

I often think about the first 11-years of Hansen’s under Randy and Hilton’s leadership. A mediocre looking business with a mediocre looking management team running a $40 million market cap. The business grew from $21 million in sales to $93 million but the business wasn’t showing any operating leverage. I’m sure many of us would have looked at the company and said, “This is a loser”.

The funny thing is we all have at least one of these companies in the portfolio. A company you’ve held onto far too long - hoping that a new product or strategy will completely change the trajectory of the company.

A Price/Earnings (PE) ratio is a good sentiment indicator. When a PE is high, expectations are high. When a PE is low, expectations are low. From 2000-2002, Hansen Natural was trading at a 10 PE. No one was expecting anything.

But then lightning struck.

In late 2002 the company launched the Monster Energy Drink with the tagline “Unleash the Beast”. The edgy packaging was the opposite of the company’s natural product offerings. They snagged some key sports sponsorships. In just two years they were able to acquire 18% market share in the $2 billion energy drink market (Red Bull held 50%).

By the end of 2004, the business grew to $180 million in sales with $20.4 million in earnings and the stock unleashed the beast. Hansen Natural was now a $350 million market cap.

In 2004 and 2005 the energy drink market soared 63%. Coca Cola and Pepsi launched several products into the category to take advantage of the market growth while their core soft drink market declined. Hansen’s Monster brand exploded.

In 2005, Hansen’s sales almost doubled to $350 million, and earnings tripled to $60 million. By the end of 2005, Hansen’s market cap grew to $2 billion. Hansen’s stock rose 3,000% in three years.

Some of you are now thinking of some loser in your portfolio thinking it could be the next Monster Beverage:

This is the interesting part – both Rodney Sacks and Hilton Schlosberg sold 40% of their holdings between 2003-2005. Could you blame them? They sat on dead money for 11-years and then the stock rips 30x. At the same time industry behemoths Coke and Pepsi were launching numerous products playing catchup. You would have sold too.

Sacks and Schlosberg didn’t know the stock would go up another 14,000% over the next 20 years. What you find is even the people closest to the business don’t even know the future.

87% of all global equities that went up 1000% or more over the past ten years were microcaps.

In 2012, Hansen Natural would change their name to Monster Beverage. In 2015, Monster Energy and Coca-Cola executed a strategic asset swap, with Coca-Cola acquiring Hansen’s juice brands while Monster gained Coke’s energy drink line. Monster consolidated its position in the energy drink market, and Coca-Cola expanded its fruit juice empire.

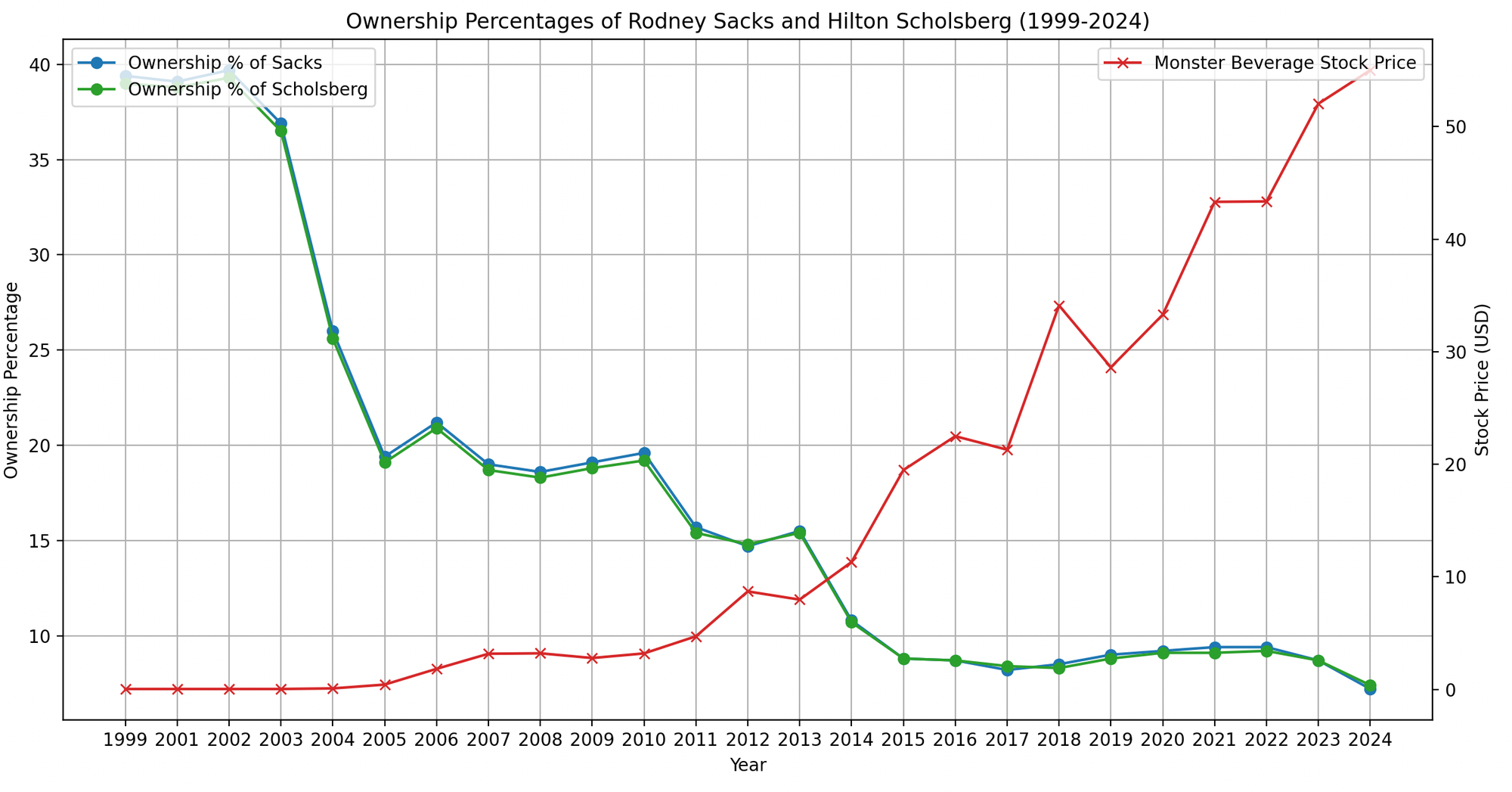

Today Rodney Sacks (74) and Hilton Schlosberg (72) are still the co-CEOs of Monster Beverage. The two co-founders would continue to sell stock rather consistently. Today they each own ~7% of the company and are both billionaires.

Here is a chart showing Rodney Sacks and Hilton Schlosberg ownership % overlayed over the stock price:

Peter Lynch famously said, "insiders might sell their shares for any number of reasons, but they buy them for only one: they think the price will rise."

Investors love insider buying. It’s the purest signal. What most investors get wrong is believing insider selling is always negative. 95% of insider selling is a non-event and offers little to no signal. Especially in microcap where most operators aren’t filthy rich. They still have bills to pay, tuition to pay, memories they need to pay for at a future Lakehouse with their kids/grandkids. Selling a little along the way doesn’t make them any less motivated.

As yourself – if you were a public CEO, would owning 10%, 30%, even 50% less stock make you any less motivated? I don’t think so. Wouldn’t the shame of a poor public track record be motivation enough? The entire executive management team, employee stock option plan, everyone’s livelihood depends on your decision making. Like all things it all comes down to character and finding and investing in good people.

Here is a great post on X that didn’t get enough attention:

Investors want managers to have "skin in the game."

— PEoperator (@PEoperator) August 23, 2024

As a manager, I want the same. I want the opportunity to bet on myself.

But the evaluation of "skin in the game" isn't as simple as what % of a manager's net worth is tied up in the company, cash comp, or how much of the… pic.twitter.com/ifJ15cpHP7

Every monster winner had a breakthrough moment - a new product, FDA approval, a big contract/customer, a super accretive acquisition, a new CEO/management team, or simply being in the right place at the right time with the right product (a little bit of luck). 80% of successful microcap investing is figuring out if a breakthrough moment is the tip of the iceberg or the whole iceberg. Can they parlay this one big win that will last for quarters into many more wins that can last for years/decades?

Every monster winner doesn’t fit perfectly into any framework. We try to cut through the noise by talking about a long-term CAGR, “Monster Beverage has produced a 26.5% CAGR over the last 32 years.” The issue with CAGR’s is it smooths over all the breakthrough moments, missed expectations, volatility, and mediocre moments. It smooths over and hides all the important lessons that need to be learned.

If you liked this article, you would also enjoy the presentation:

Interact and learn with 250+ of the best microcap investors on the planet:

MicroCapClub is an exclusive forum for experienced microcap investors focused on microcap companies (sub $500m market cap) trading on United States, Canadian, European, and Australian markets. MicroCapClub was created to be a platform for experienced microcap investors to share and discuss stock ideas. Since 2011, our members have profiled 1000+ microcap companies. Investors can join our community by applying to become a member or subscribing to gain instant view only access. MicroCapClub’s mission is to foster the highest quality microcap investor Community, produce Educational content for investors, and promote better Leadership in the microcap arena. For more information, visit https://microcapclub.com/ and https://microcapclub.com/summit/